Table Of Content

Check out our affordability calculator, and look for homebuyer grants in your area. Visit our mortgage education center for helpful tips and information. And from applying for a loan to managing your mortgage, Chase MyHome has you covered. Conforming loans are bought by housing agencies such as Freddie Mac and Fannie Mae and follow their terms and conditions.

Buying Options

If one month the cost of a movie ticket edges your budget into the red you can skip it. Depending on your insurance coverage, and how often you find yourself in a doctor’s waiting room, healthcare will impact your cost of living differently each year. Overall, transportation expenses in Los Angeles, CA, are 26 percent above the national average. This is consistent with other cities about the same size and includes maintenance costs and gas. With these particular utility needs, expect to pay about $207.75 per month on total energy costs. Making housing costs even more challenging, nearby cities don’t often cut you a break, either.

How to calculate annual income for your household

Private Mortgage Insurance (PMI) is calculated based on your credit score and amount of down payment. If your loan amount is greater than 80% of the home purchase price, lenders require insurance on their investment. If you are taking out a conventional loan and you put down less than 20%, private mortgage insurance will take up part of your monthly budget. The PMI’s cost will vary based on your lender, how much money you end up putting down, as well as your credit score. It is calculated as a percentage of your total loan amount, and usually ranges between 0.58% and 1.86%. In 2019, the average annual cost of homeowners insurance was $1,083 nationwide.

Rocket Sister Companies

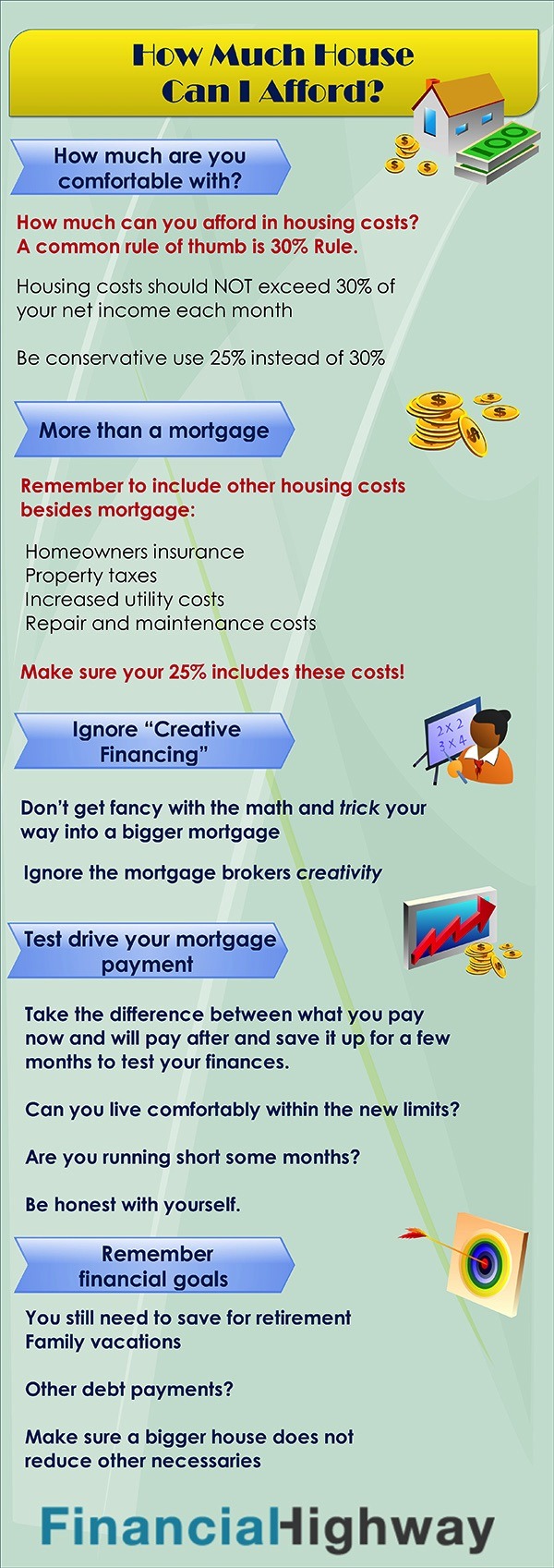

That means your monthly home payment will be the same, even for long-term loans, such as 30-year fixed-rate mortgages. Two benefits to this mortgage loan type are stability and being able to calculate your total interest on your home upfront. Use this tool to calculate the maximum monthly mortgage payment you'd qualify for and how much home you could afford. An optimal DTI is 36% or below, including possible housing costs, but excluding current rent payments, if any. If your monthly income is, for example, $5,000, then you shouldn’t owe more than $1,800 per month. USDA loan terms for qualifying rural areas are much more flexible than regular loans.

Best Neighborhoods to Buy a House in the Los Angeles Area

You might find that you don’t want to buy the most expensive home that fits in your budget. Banks don’t like to lend to borrowers who have a low margin of error. That’s why your pre-existing debt will affect how much home you qualify for when it comes to securing a mortgage. Before you start looking at real estate and shopping around for the right lender, it’s important to take these steps to improve your chances of becoming a homeowner without breaking the bank.

'I shouldn't be punished': My sister can't afford to buy me out of our mother's $450,000 house. She has no home. What ... - Yahoo Finance

'I shouldn't be punished': My sister can't afford to buy me out of our mother's $450,000 house. She has no home. What ....

Posted: Sat, 10 Feb 2024 08:00:00 GMT [source]

How to improve your home affordability

The "principal" is the amount you borrowed and have to pay back (the loan itself), and the interest is the amount the lender charges for lending you the money. Most lenders want you to have a credit score of at least 620 to get a conventional loan. However, it is possible to get a mortgage with a bad credit score, but you will have to put more money down or pay a higher interest rate. A key factor in whether or not you can afford a home is based on the mortgage rate offered. And with current mortgage rates doubling in 2022, it has been a top factor in slowing down home purchases heading into 2023. Even a few basis points can make the difference between a home being affordable or out of reach (a basis point equals one-hundredth of a percentage point).

So don’t feel like you’re stuck with the rate of the first lender you meet. Many lenders use this ratio to determine if you can afford a conventional home loan without putting a strain on your finances or causing you to go into default. The 28/36 rule also protects borrowers as much as it protects lenders, as you’re less likely to lose your home to foreclosure by overspending on a home. This loan is a great option for anyone who is a veteran or currently serving in the United States military. The loan does not require any down payment, and unlike other loans, it also does not require private mortgage insurance.

Income

You can get a conventional loan (a loan not backed by a government agency) for as little as 3% down. The Rocket Mortgage® Home Affordability Calculator gives you the option to see how much house you can afford, or how much cash you need for your down payment and closing costs. Read more on specialized loans, such as VA loan requirements and FHA loan qualification. In addition, take a look at the best places to get a mortgage in the U.S.

Check the county assessor’s website and local real estate listings to get an accurate idea of the property tax rates in the area where you’re buying. Nationwide, rates range from 0.30% to 2.13% of the home’s assessed value. Assessed value may be lower than market value, thanks to homestead exemptions. The best-case scenario is getting the seller to pay closing costs without increasing the purchase price. It may be hard to get this concession in a seller’s market, but it may be doable in a buyer’s market. Once you can put down 20%, you won’t have to pay for mortgage insurance.

Department of Agriculture and offer certain benefits that conventional loans don’t. Borrowers with a credit score of 580 and above could also pay as little as 3.5% as a down payment, lower than the typical 10% or higher with a non-FHA loan. Keep in mind that there are other loan types you may qualify for that have fewer restrictions and provide other benefits.

Perhaps you need to make a budget and a plan to knock out some of your large student or car loans before you apply for a mortgage. Or you wait until you get a raise at work or change jobs to apply for a mortgage. In the case of a 30-year mortgage (depending, of course, on the interest rate) the loan’s interest can add up to three or four times the listed price of the house (yes, you read that right!). For the first 10 years of a 30-year mortgage, you could be paying almost solely on the interest and hardly making a dent in the principal on your loan. Borrowers who have served or have certain military connections may qualify for a VA loan. They are backed by the Department of Veterans Affairs and typically don’t require a down payment.

It’s a big responsibility that ties up a large amount of money for years. That’s why it can make a significant difference if you make even small extra payments toward the principal, or start with a bigger down payment (which of course translates into a smaller loan). Perhaps more importantly, however, you avoid putting yourself at the limits of your financial resources if you choose a house with a price lower than your maximum. But beyond that you’ve got to think about your lifestyle, such as how much money you have leftover for travel, retirement, other financial goals, etc.

No comments:

Post a Comment